Seeking Assistance from a Mediator to Develop a QDRO

A qualified domestic relations order (QDRO) is a separate order from the court that explains how a retirement account is split by a couple at divorce. A QDRO contains specific language and terms that instruct the plan administrator how to divide it and treat it after divorce. The terms must comply with the retirement plan’s guidelines.

A qualified domestic relations order (QDRO) is a separate order from the court that explains how a retirement account is split by a couple at divorce. A QDRO contains specific language and terms that instruct the plan administrator how to divide it and treat it after divorce. The terms must comply with the retirement plan’s guidelines.

QDROs make up an important part of the process of dividing assets. Retirement accounts may represent the largest asset a couple has. It is given certain protection by law that may not be attached to other types of assets. Until 1984, a retirement account was not subject to division in a divorce. A QDRO must be carefully drafted. It cannot require the plan administrator to pay the other spouse more than, sooner than or in a different manner than the spouse whose name the account is titled in can receive payments.

A mediator can help a couple determine terms for their QDRO. There may be many options for the division, such as making a lump-sum payment, paying a monthly payment in retirement years, being made into new retirement accounts or other arrangements. A skilled mediator can walk through each option with the parties. He or she can learn what the interests of the parties are and work on an agreement that protects the interests of both parties. In some cases, a 50/50 split is fair. In other situations, the parties may agree to divide other property differently to decrease the total retirement benefits the non-participating spouse receives.

A mediator can also consider the tax effects of different arrangements and can offer recommendations on how to minimize the amount of taxes that are incurred due to the division of the account. If drafted properly, a QDRO can help avoid a tax penalty for early distribution.

Arbitration and Mediation of Bad Faith Insurance Claims

A bad faith insurance claim may arise if an insurance company is accused of wrongful conduct, that is unreasonable or malicious, fraudulent or oppressive. These claims may arise when an insurance company refuses to pay benefits for a valid claim. If there is malicious conduct, this may expose the insurance company to having to pay punitive damages if the claim against it is proved.

A bad faith insurance claim may arise if an insurance company is accused of wrongful conduct, that is unreasonable or malicious, fraudulent or oppressive. These claims may arise when an insurance company refuses to pay benefits for a valid claim. If there is malicious conduct, this may expose the insurance company to having to pay punitive damages if the claim against it is proved.

The parties involved in a dispute of this nature may decide to try to resolve it through mediation or arbitration. In mediation, the mediator does not have authority to impose a decision on the parties. The mediator’s role is to help the parties reach an agreement together. In arbitration, the arbitrator conducts a hearing similar to a litigated case. He or she renders a legally-binding decision.

Arbitration proceeds much like a typical court case. Each side can call witnesses, present evidence and make arguments through their attorney. Mediation is more informal in nature and often levels the playing field between parties who may be on different power levels.

Both forms of alternative dispute resolution have advantages over traditional litigation. Mediation and arbitration are both confidential processes. Either one can help avoid the bad publicity potential that arises with litigation. This may be an important consideration in a bad faith case. Both processes are usually able to wrap up the case in far less time than litigation would entail. In litigation, it may take substantial time to convince an insurance company of the merits of the case. It must often be convinced that the denial of the claim was wrong. Mediation or arbitration may get the insurance company to accept this in a way that litigation might not. In some situations, the insurance company may agree to pay on the original claim to avoid the furtherance of a bad faith claim.

Robert S. Bernstein

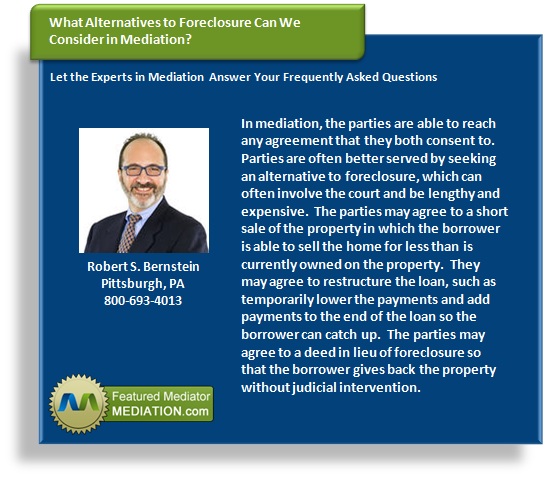

What Happens at Foreclosure Mediation?

More banks, lenders, borrowers and others are turning to the process of mediation in foreclosure cases. These cases often involve significant assets, likely the most expensive asset one of the parties owned. The stakes are often high and both parties may be incentivized to avoid the lengthy and expensive foreclosure process.

More banks, lenders, borrowers and others are turning to the process of mediation in foreclosure cases. These cases often involve significant assets, likely the most expensive asset one of the parties owned. The stakes are often high and both parties may be incentivized to avoid the lengthy and expensive foreclosure process.

Every mediation is unique because different parties and interests are involved. However, they may follow a similar process. Many mediation sessions begin with a join session in which all of the parties, their attorneys and other interested persons are present. The mediator begins by explaining the rules of mediation and the process. Each side of the issue has their turn to discuss their position. The parties may speak directly to each other at this process.

From there, mediation may proceed in a joint session or the parties may break into private caucuses. During these private caucuses, the parties share information with the mediator who then funnels information back and forth between the parties. The mediator may provide additional information about the process of foreclosure and the disadvantages of not reaching an early intervention in the case. He or she also communicates offers and counteroffers between the parties.

During the private caucuses, the mediator also tries to identify the interests of the parties so that he or she can propose possible solutions that will satisfy both sets of interests. For example, the borrower may accept that he or she can no longer afford the property but may want to delay a moving date. The lender may want to avoid having to go to court. The mediator can propose solutions to the parties as well as ask them to generate ideas during a joint brainstorming session.

If the parties reach an agreement, they usually enter into a separate binding agreement.

David A. Simson

October 8, 2018

Why Prenuptial And Postnuptial Agreements Lead To Stronger Marriages And Prevent Disastrous Divorces – You can’t predict the future. The hard truth is that the way you feel about your partner today may not be the way you feel as life evolves. Marriage is wonderful. Marriage is difficult. That is why it is so important to have level-headed discussions about what might happen if your feelings change in the future now, when you are sitting on the same side of the table and both truly want what is best for each other.

Record Corporate Debt And The Next Financial Crisis: 5 Things Investors Need To Know – It’s been 10 years since the worst financial crisis the Great Depression tanked the world economy and wiped out $34 trillion in global equity market capitalization.

What to consider when buying a home amid rising mortgage rates – Many economists say mortgage rates will continue to trend upward this year and peak around 5 percent at most, which is still below average. Mortgage rates averaged consistently above 10 percent every year between 1979 and 1990 and then eased down to a range from 6 to 8 percent between 1992 and 1998, according to Freddie Mac’s records.